Factor Modeling

Max Margenot

Lead - Data Science at Quantopian

This presentation is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security; nor does it constitute an offer to provide investment advisory or other services by Quantopian, Inc. ("Quantopian"). Nothing contained herein constitutes investment advice or offers any opinion with respect to the suitability of any security, and any views expressed herein should not be taken as advice to buy, sell, or hold any security or as an endorsement of any security or company. In preparing the information contained herein, Quantopian, Inc. has not taken into account the investment needs, objectives, and financial circumstances of any particular investor. Any views expressed and data illustrated herein were prepared based upon information, believed to be reliable, available to Quantopian, Inc. at the time of publication. Quantopian makes no guarantees as to their accuracy or completeness. All information is subject to change and may quickly become unreliable for various reasons, including changes in market conditions or economic circumstances.

Background¶

- Me

What is a Factor?¶

Some value assigned to a security in a universe.

They come in two flavors, Alpha and Risk.

Popularity of Factor Models¶

"Smart Beta" Portfolios

87% of institutional investors incorporating factors into investment process*

67% of into risk management process*

53% of into investment strategies*

*"The rise of factor investing." BlackRock. 7 Apr. 2017

Goals of Factor Models¶

Diversify with specific premia.

Analyze risk.

Increase returns.

Common Factor Portfolios¶

Most factors fall into one of five categories:

Value

Momentum

Quality

Volatility

Growth

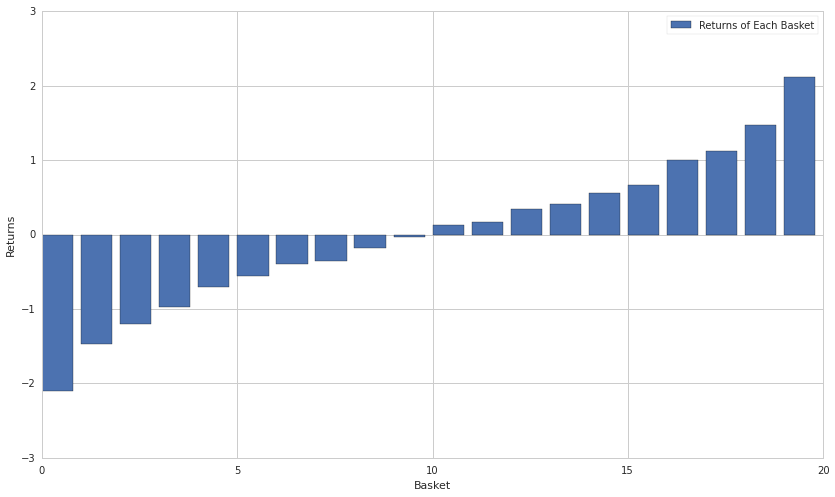

Portfolio Construction¶

Cross-Sectional Equity:

Rank all securities in your universe from lowest factor exposure to highest.

Go long on the top percentile.

Go short on the bottom percentile.

The Universe¶

Sufficient liquidity.

No "hard-to-trade" securities.

universe = QTradableStocksUS()

Example Factor: Momentum¶

class Momentum(CustomFactor):

""" Momentum factor """

inputs = [USEquityPricing.close,

Returns(window_length=126)]

window_length = 252

def compute(self, today, assets, out, prices, returns):

out[:] = ((prices[-21] - prices[-252])/prices[-252] -

(prices[-1] - prices[-21])/prices[-21]) / np.nanstd(returns, axis=0)

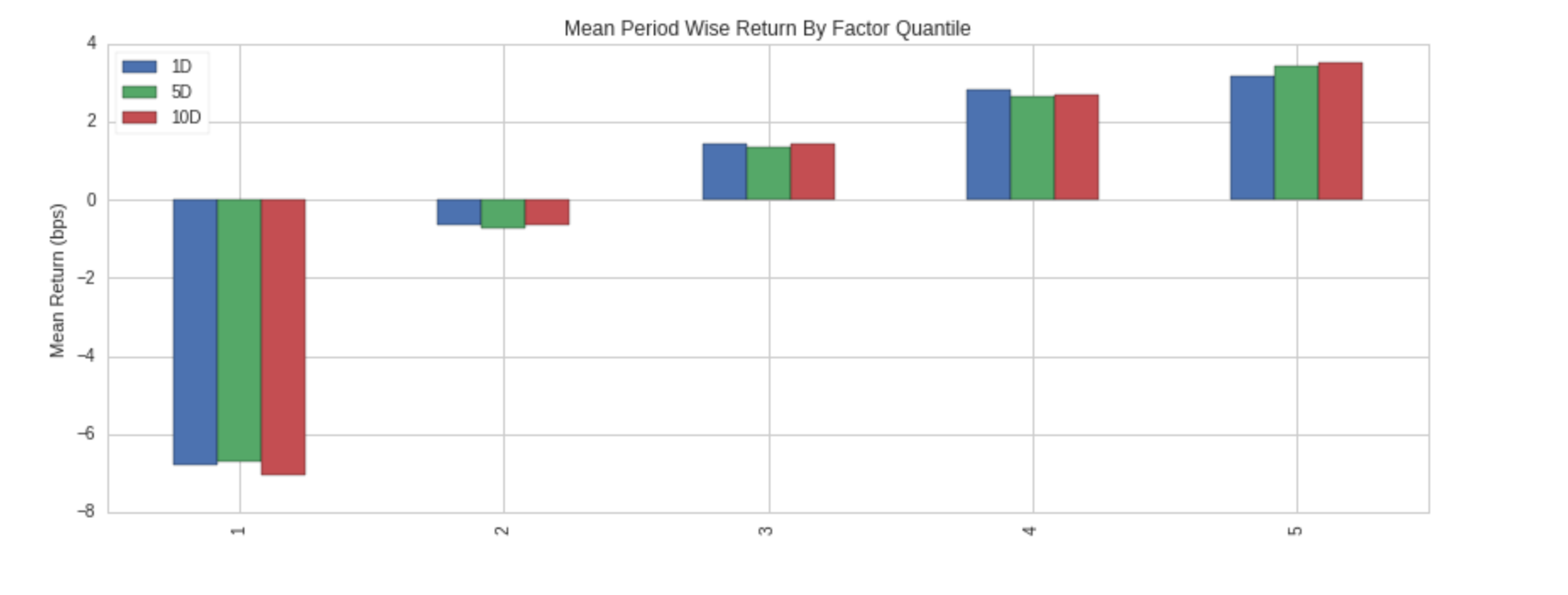

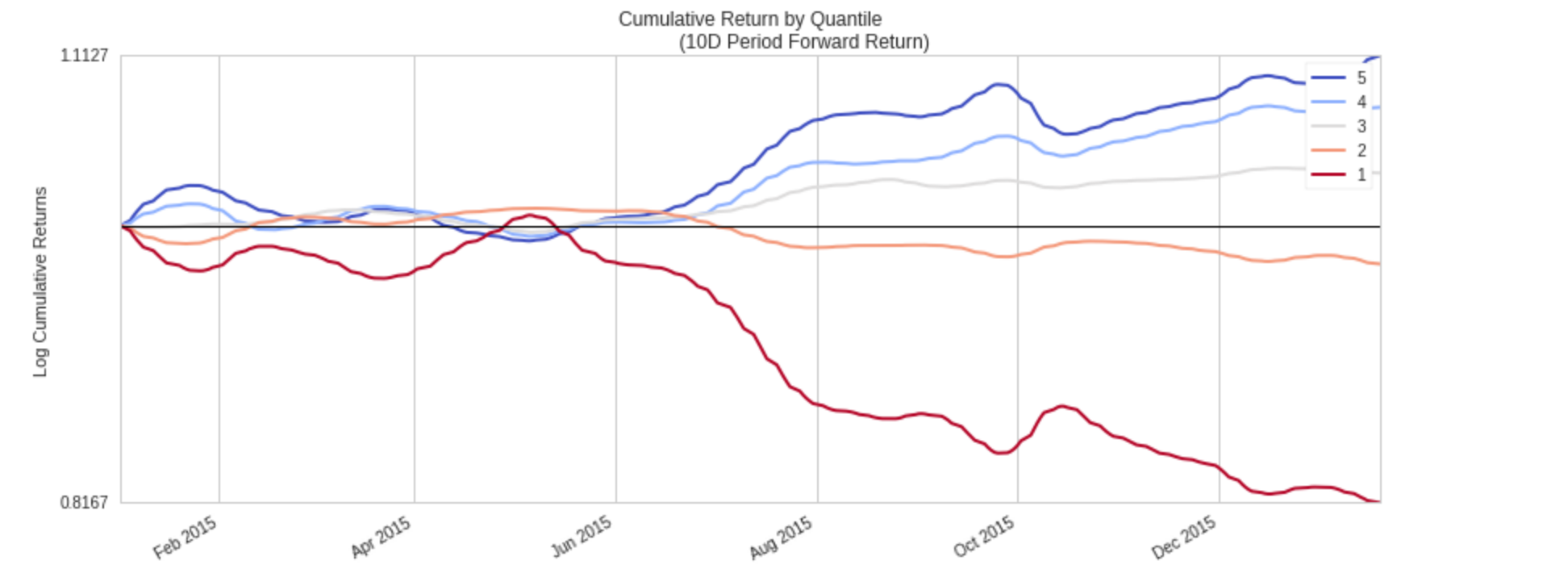

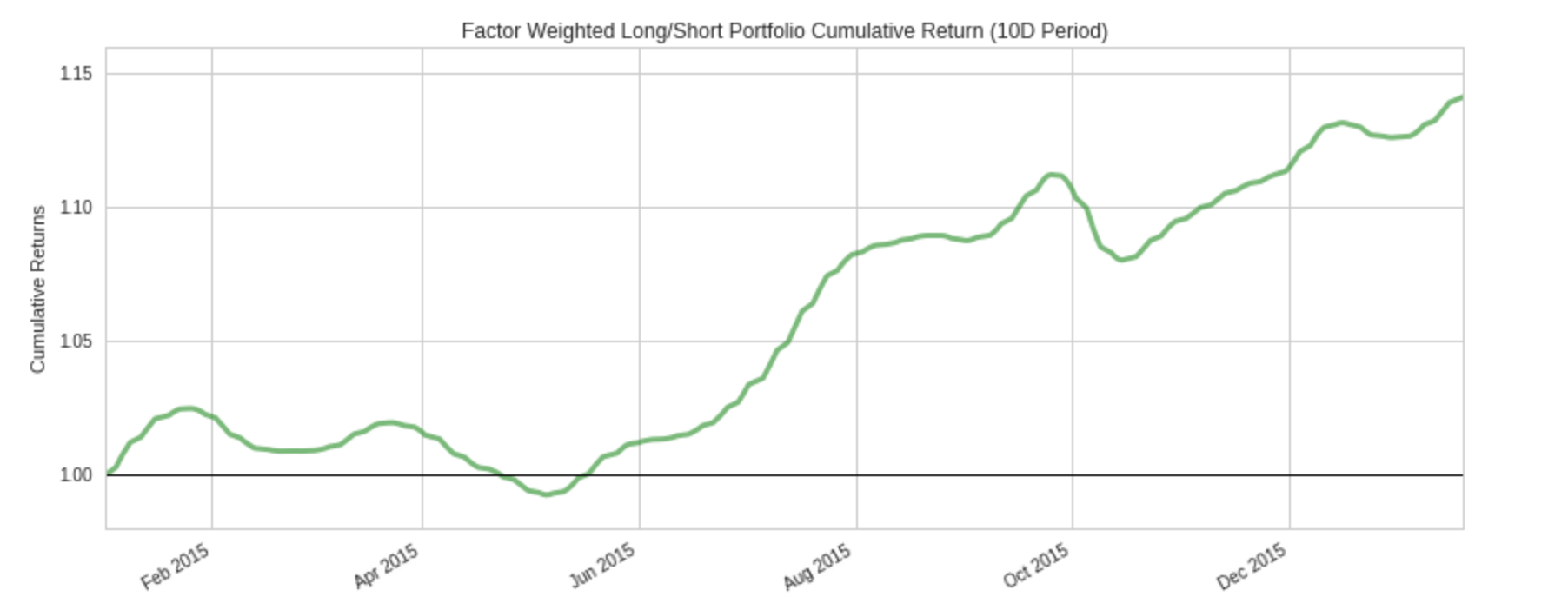

Example Factor: Momentum¶

Example Factor: Momentum¶

Example Factor: Momentum¶

Why Use This Method?¶

Predicting prices is hard.

With factor modeling, we capture the relative value of the long and short baskets.

Key implied assumption is that the expected return of each security is proportional to its factor value.

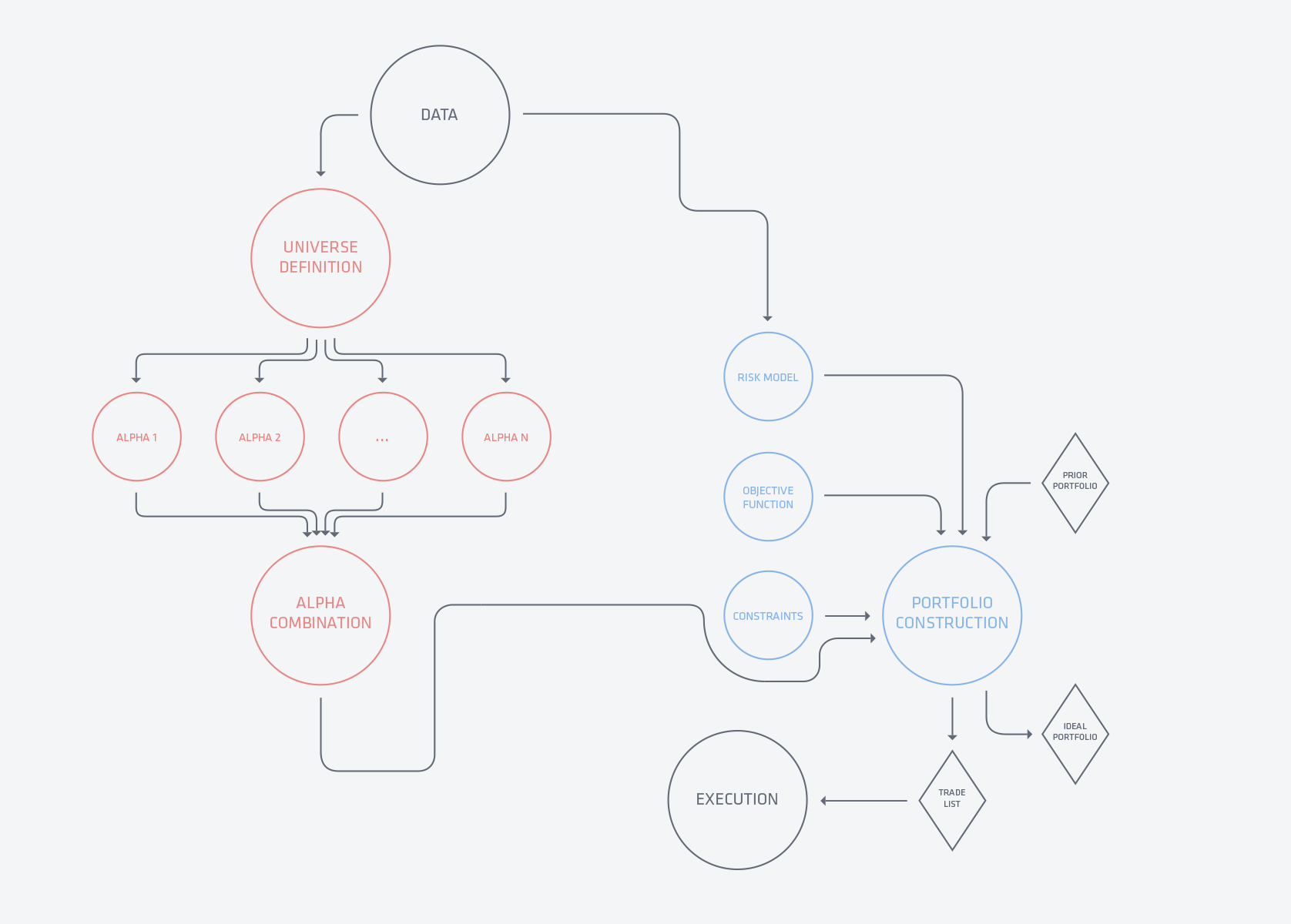

The Quant Workflow¶

Alpha and Risk¶

Typical form of constructing any sort of factor portfolio.

How do we distinguish between Alpha and Risk?

Portfolio Diversification¶

Company-level risks disappear, but larger common factors remain.

We can define these common factors however we like.

Capital Asset Pricing Model¶

Uses the market at large as a single common risk factor:

$$ r_p = \alpha + \beta_{m} r_{m} $$

Fama-French Factors¶

Add additional common factors to the base CAPM:

$$ r_p = \alpha + \beta_{m} r_{m} + \beta_{hml} r_{hml} + \beta_{smb} r_{smb} $$

General Factors¶

We can extend this as far as we want:

$$ r_p = \alpha + \beta_0 r_0 + \cdots + \beta_n r_n $$

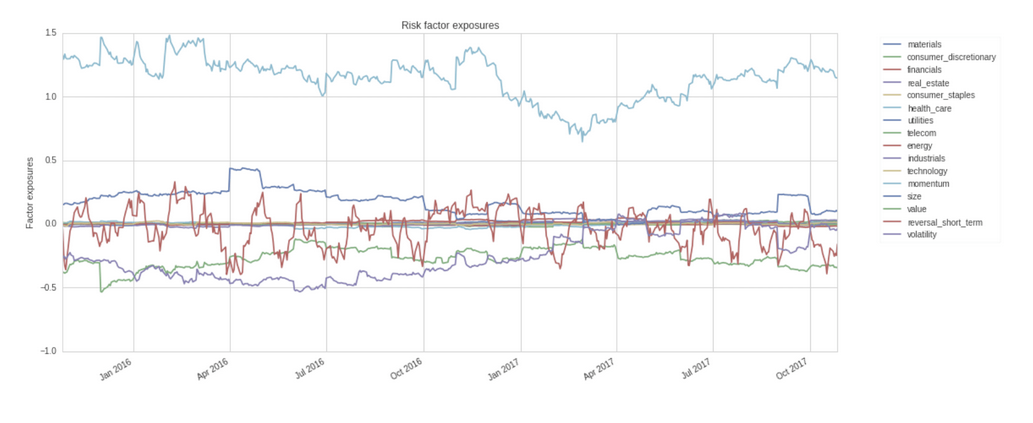

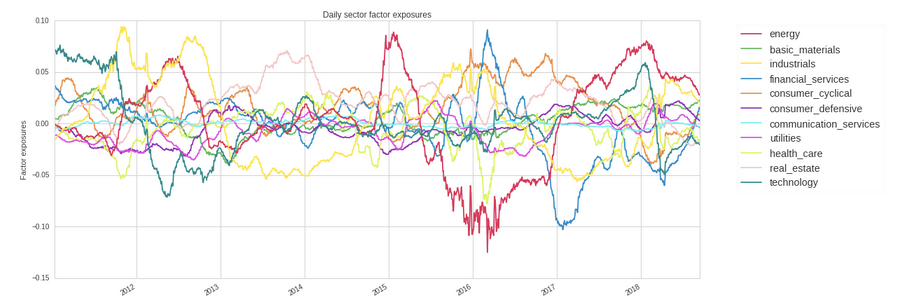

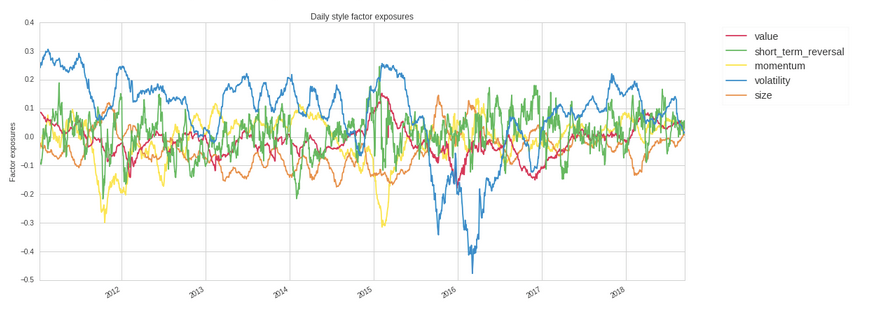

Quantopian Risk Model¶

Sectors¶

Styles¶

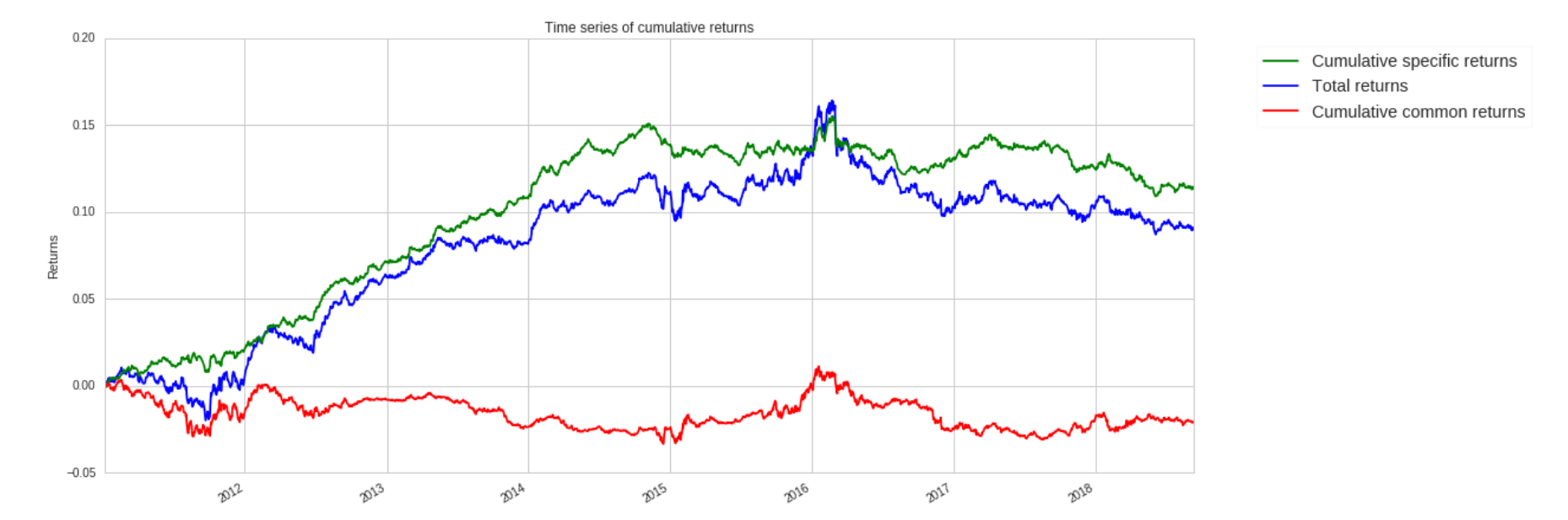

Performance Attribution¶

Alpha¶

Alpha is what remains after you have removed all common factor risk.

It can only be defined in terms of what you don't want.

Finding Alpha¶

A very difficult problem.

To find a reliable source of alpha, you must have a clearly defined set of common factor risks.

Alpha decays.

Tools¶

- Alphalens: https://github.com/quantopian/alphalens

- Pyfolio: https://github.com/quantopian/pyfolio

- Zipline: https://github.com/quantopian/zipline

References¶

Quantopian Lecture Series - https://quantopian.com/lectures

Quantopian Risk Model - https://www.quantopian.com/papers/risk

@clean_utensils

@mmargenot

max@quantopian.com

Enter the Quantopian Daily Contest at www.quantopian.com/contest

This presentation is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security; nor does it constitute an offer to provide investment advisory or other services by Quantopian, Inc. ("Quantopian"). Nothing contained herein constitutes investment advice or offers any opinion with respect to the suitability of any security, and any views expressed herein should not be taken as advice to buy, sell, or hold any security or as an endorsement of any security or company. In preparing the information contained herein, Quantopian, Inc. has not taken into account the investment needs, objectives, and financial circumstances of any particular investor. Any views expressed and data illustrated herein were prepared based upon information, believed to be reliable, available to Quantopian, Inc. at the time of publication. Quantopian makes no guarantees as to their accuracy or completeness. All information is subject to change and may quickly become unreliable for various reasons, including changes in market conditions or economic circumstances.